TL;DR

Impact reporting is the practice of showing, with evidence, how an organization’s actions affect people, society, and the environment. A strong impact report goes beyond listing activities. It combines data, stories, honest acknowledgment of gaps, and clear next steps. Organizations that treat impact reporting as a proof system (not a highlight reel) build more trust with investors, donors, customers, and partners.

Impact Reporting in 2026: At a Glance

Impact reporting is the evidence-based communication of an organization’s social and environmental effects. In 2026, it has transitioned from voluntary storytelling to a structured data requirement.

The Framework: A credible impact report follows the Claim-Proof-Context framework, measuring outcomes (actual change) rather than just outputs (activities).

The Regulation: For EU-regulated firms, this is now largely governed by the CSRD and ESRS standards, emphasizing "double materiality" and quantitative transparency.

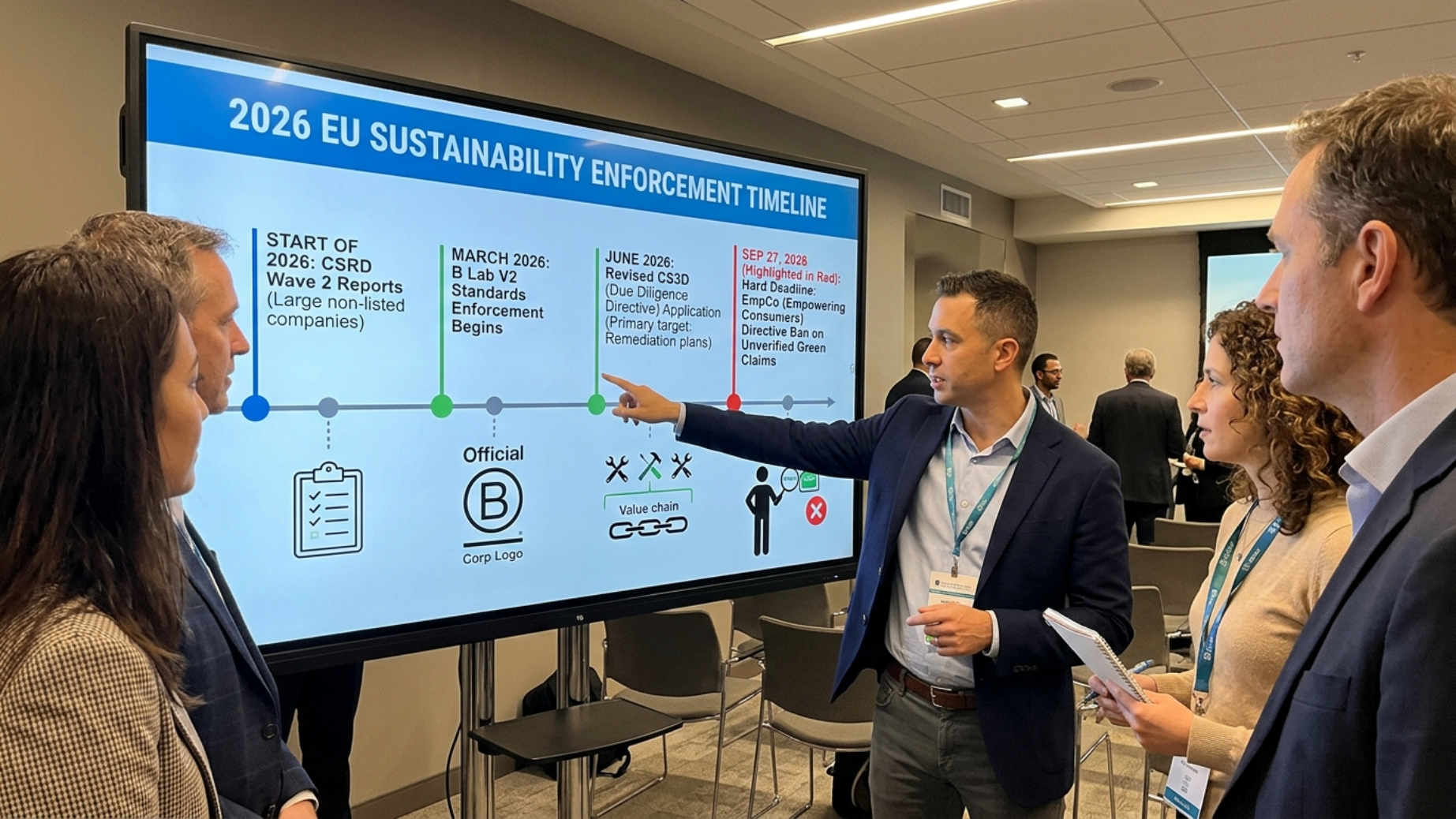

The Deadline: Under the Empowering Consumers Directive (EmpCo), binding rules for all sustainability claims enter into force on September 27, 2026.

What Is Impact Reporting?

Impact reporting is the process of measuring, interpreting, and communicating the real effects an organization has on people, communities, the environment, and sometimes business performance. It usually produces an impact report: a stakeholder-facing document that explains what the organization set out to do, what it actually did, what changed, how the change was measured, what challenges remain, and what comes next.

The format varies. An impact report can be a designed PDF, an interactive webpage, a board deck, a donor update, a dashboard, or a short video. What matters is not the container but whether the content is specific, evidence-backed, and honest about limitations.

The Global Impact Investing Network (GIIN) defines impact as a change in an important positive or negative outcome for people or the planet, and recommends evaluating it across five dimensions: what changed, who experienced it, how much occurred, the organization’s contribution, and the risk that impact does not materialize as expected. GIIN IRIS+ provides a useful starting framework for anyone building an impact reporting practice from scratch.

One important distinction: impact reporting is the communication process. Impact measurement is the data collection and analysis that feeds it. Impact management goes further, using findings to improve decisions and strategy. Many organizations conflate these terms, which creates confusion before the first draft is even written.

Why Impact Reporting Matters

Stakeholders no longer accept vague purpose language. They want proof.

Stakeholder confidence remains a challenge. According to the PwC 2025 Global Investor Survey, 87% of investors now specifically scrutinize AI-related impact performance alongside traditional climate data. This reflects a growing demand for transparency in how automated systems affect labor and data privacy, moving beyond the 94% "trust gap" noted in previous years.

Consumers are watching too. PwC’s Consumer Intelligence Series found that 76% of consumers said they would stop buying from companies that treat employees, communities, and the environment poorly. When a brand publishes credible impact data, it gives customers a reason to stay. When it publishes vague claims, it gives them a reason to leave.

Beyond trust, impact reporting drives better internal decisions. Organizations that track outcomes (not just activities) learn what works, what doesn’t, and where to invest next. The report becomes a decision-making tool, not just a communication piece. This is where the real value sits: turning evidence into action that improves both impact and commercial performance.

For purpose-driven brands trying to connect sustainability work to actual business results, a well-built impact report is the bridge between brand activation strategy and stakeholder confidence.

What Does an Impact Report Include?

The simplest structure answers six questions: What problem were you trying to address? What did you do? Who was affected? What changed? How do you know? What will you do next?

Here is what the core sections typically look like:

Executive summary. Headline progress, biggest lesson, top metrics, and next priorities. Put the most important information first because many readers will skim.

Purpose and scope. What the report covers, the reporting period, which programs or business units are included, and what is excluded (with a reason).

Problem or need. The social, environmental, or stakeholder issue being addressed. Start with the “why” before the “what.”

Goals and commitments. What the organization said it would do, and the targets it set. Botanical PaperWorks’ CEO shared on LinkedIn that the company’s first annual impact report used a “what we said we’d do” vs. “what we did” structure, which took about three months from start to finish partly because they needed to finalize their carbon emissions methodology.

Metrics and results. Quantitative outcomes, qualitative evidence, baselines, year-over-year comparisons, and methodology notes.

Stories and stakeholder voices. Beneficiary stories, customer insights, employee voices, and partner testimonials paired with data.

Challenges and gaps. Missed targets, incomplete data, negative impacts, trade-offs, and what did not work. This section is what separates a credible report from marketing collateral.

Future commitments. What happens next, how the organization plans to improve measurement, and how stakeholders can participate.

Methodology appendix. Definitions, data sources, calculation methods, assurance statements, and framework references for readers who need the detail.

The Impact Ladder: Activities Are Not Outcomes

One of the most common mistakes in impact reporting is treating activity counts as proof of impact. Hosting 12 workshops is an activity. Reaching 500 people is an output. Seeing 70% of participants change a specific behavior is an outcome. Measuring a sustained reduction in harm over time is impact.

Level | Question | Example |

|---|---|---|

Input | What resources did we invest? | $50,000 and 200 staff hours |

Activity | What did we do? | Hosted community workshops |

Output | What was produced? | 500 participants attended |

Outcome | What changed? | 68% adopted target behavior |

Impact | What longer-term difference resulted? | Measurable reduction in waste over 12 months |

Most “impact reports” actually report outputs and outcomes. That is acceptable, as long as the labels are honest. The problem is when organizations call outputs “impact” without evidence of actual change.

Practitioners on Reddit consistently call this out. In one nonprofit thread, a commenter distinguished between an annual report that lists activities and a true impact report that needs outcome data and stories, advising organizations to report changes in food security rather than just meals served. The same thinking applies to brands: reporting “percentage of packaging converted to recyclable formats” is more meaningful than reporting “number of sustainability meetings held.”

For brands and retailers, useful metrics include purchase intent shifts, sustainable product adoption rates, packaging weight reduction, recycled material percentages, and shopper behavior data from sustainability market research. The key is measuring what actually changed, not what the organization was busy doing.

Impact Reporting vs. ESG, Sustainability, CSR, and Annual Reporting

These terms overlap but are not interchangeable.

Sustainability reporting uses standards like GRI or ESRS to cover impacts on the economy, environment, and people. The GRI Standards provide a structured approach, often broader and more compliance-oriented than impact reporting.

ESG reporting focuses on environmental, social, and governance risks and performance, typically for investors and regulators. It can prioritize enterprise risk over real-world outcomes.

CSR reports describe corporate social responsibility programs. The framing is older and often focuses on initiatives rather than measurable change.

Annual reports cover financial and operational performance. They may include impact data, but an impact report should go deeper on outcomes and learning.

Benefit reports are required for some benefit corporations depending on jurisdiction and legal form.

Impact reporting is the broadest and most flexible of these. It can be public or internal, donor-facing or investor-facing, standards-aligned or narrative-led. The format depends on the audience and the decision the report needs to support.

Is Impact Reporting Mandatory?

It depends. The EU’s Corporate Sustainability Reporting Directive (CSRD) requires companies above a certain size to disclose sustainability risks, opportunities, and impacts using European Sustainability Reporting Standards. The first companies applied these rules for the 2024 financial year.

Certified B Corps must now adhere to the B Lab Standards V2, which became fully operational in early 2026. This version represents a structural shift: it replaces the flexible 80-point threshold with mandatory minimum requirements across seven core Impact Topics, including Climate Action, JEDI (Justice, Equity, Diversity, and Inclusion), and Fair Work. Continuous improvement milestones are now a prerequisite for recertification.

Feature | Pre-2026 Standard | 2026 Standard (Current) |

B Corp Threshold | 80-point cumulative score | Mandatory Minimums (7 Topics) |

Investor Focus | Climate & Carbon only | Climate + AI & Tech Ethics |

EU Enforcement | Transition Plan focus | Identification & Remediation (CS3D) |

Primary Regulation | Voluntary/GRI | Mandatory CSRD / ESRS |

For many organizations, impact reporting is voluntary but increasingly expected by funders, investors, customers, partners, and procurement teams. KPMG’s 2024 Survey of Sustainability Reporting found that 100% of surveyed U.S. businesses now report ESG metrics, and a growing majority obtain third-party assurance. Even where it is not legally required, impact reporting is becoming a baseline expectation.

While the CSRD remains the primary "stick" for disclosure, the Corporate Sustainability Due Diligence Directive (CS3D) was restructured in 2026. The current enforcement focus has shifted significantly toward active identification and remediation of value chain harms, rather than just the publication of transition plans.

The 2026 Regulatory Landscape: CSRD & The Omnibus I Directive

As of March 2026, the EU’s Omnibus I Directive has entered into force, streamlining reporting for smaller enterprises. While reporting is mandatory for large firms, the 2026 updates prioritize quantitative data over narrative and have introduced a "value-chain cap" to prevent large corporations from overburdening their SME partners with data requests.

Key 2026 Deadlines & Thresholds:

Company Category | Employee Count | Revenue Threshold | 2026 Status |

Large EU Companies | > 500 | €50M+ | Full CSRD Compliance Required |

Mid-Market Firms | 250 - 500 | €40M - €50M | First reports due for 2025 FY |

SMEs (Listed) | < 250 | < €40M | Eligible for "Simplified ESRS" |

Emerging 2026 Trends in Impact Communication

As reporting shifts from a compliance exercise to a core business strategy, three trends are defining the 2026 landscape:

AI-Assisted Verification (Agentic AI): Organizations are moving beyond manual audits to "Agentic AI" systems. These tools can autonomously cross-reference internal supply chain logs with real-time satellite imagery and IoT sensor data to verify environmental claims (e.g., deforestation-free sourcing) in near real-time.

Double Materiality 2.0: Under 2026 ESRS updates, the focus has shifted from "Single Materiality" (financial risk to the company) to Double Materiality. This requires reporting both the "Outside-In" (financial impact) and "Inside-Out" (how the company affects the world) perspectives, ensuring that social and environmental impacts are weighted equally with financial ones.

Interactive ESG Dashboards: The era of the 100-page static PDF is ending. Investors and stakeholders now demand "Queryable Data Portals." These interactive dashboards allow users to filter data by region, business unit, or specific SDG (Sustainable Development Goal) metric, providing a more transparent and accessible view of performance.

What Makes Impact Reporting Credible?

A credible impact report follows a simple discipline: Claim, Proof, Context, Limits, Action.

Claim. What progress are you asserting? Be specific.

Proof. Which metric, story, or third-party source supports it?

Context. Compared with what baseline, target, prior year, or industry benchmark?

Limits. What does the data not prove? Where is the evidence incomplete?

Action. What will you change, improve, or investigate next?

Here is what this looks like in practice. A weak claim says: “We supported sustainable packaging and reduced waste.” A stronger version says: “In 2025, we replaced our primary packaging component with post-consumer recycled material across three product lines, reducing virgin plastic use by 14 tons compared with our 2024 baseline. We have not yet measured end-of-life recycling rates, so our next step is to work with retail partners to track disposal behavior.”

The second version is specific, measurable, contextualized, honest about gaps, and forward-looking. That is what credibility looks like.

Practitioners on LinkedIn who analyze B Corp reporting argue that credible impact reporting should inventory direct and indirect impacts, measure them, explain mitigation plans, and report progress openly, praising brands that step away from overconfident green claims. A 2026 practitioner article on B Corp materiality emphasizes that without a clear value chain, materiality becomes guesswork, and companies should identify actual impacts rather than generic topic lists.

For organizations worried about avoiding greenwashing, the rule is straightforward: if a claim cannot be supported with evidence, methodology, and context, it should not be in the report.

Common Impact Reporting Mistakes

Reporting activities as impact. Saying “we hosted 50 events” without showing what changed for participants.

Publishing a highlight reel. If the report only includes wins, stakeholders will discount it. The strongest reports show what did not work and what the organization learned.

Using undefined metrics. In a Reddit thread about a “false impact report,” practitioners emphasized that “people served” can mean unique individuals, encounters, households, or service units, and vague definitions create both confusion and ethical risk. Define every unit precisely.

Waiting until year-end to start. King’s Trust International recommends on LinkedIn that impact reporting be integrated into organizational processes throughout the year, not treated as a last-minute exercise. The data collection, methodology decisions, and staff engagement need to happen well before the designer asks for copy.

Making one report serve every audience. The better approach is a two-report model: a short, visual public report for general audiences and a detailed evidence pack for funders, investors, and scrutinizers. Unit of Impact recommends separating what you measure from what you share and providing supplemental data for stakeholders who need it.

Over-reporting relative to resources. In a recent Reddit discussion, a nonprofit staff member described extensive audit and reporting demands tied to a $25,000 grant that felt wildly disproportionate. Commenters advised weighing reporting burden against funding value before taking on grants. The depth of reporting should match the decision it supports.

How to Use an Impact Report After Publishing

The report is source material, not the final product. A well-built impact report feeds:

Website impact pages and purpose-driven brand storytelling

Investor, board, and stakeholder engagement updates

Retail sell-in decks and category stories

Donor stewardship and grant applications

Employee onboarding and internal alignment

Social media, email, and campaign content

Partnership proposals and press materials

Practitioners on Reddit report that many donors skim long reports, but major donors and funders notice organizations that provide credible reports even when not required. Think of impact reporting as trust infrastructure. Some of its value will never show up as clicks or downloads, but it shapes decisions made behind closed doors.

The organizations that get the most from impact reporting are those that treat the report as a proof library, mining it for metrics, quotes, stories, and evidence that support every stakeholder conversation throughout the year. For brands working to bridge the intention-action gap in sustainable behavior, the impact report becomes the credibility foundation for every claim made at shelf, online, or in a pitch deck.

Frequently Asked Questions

What is the difference between impact reporting and impact measurement?

Impact measurement is collecting and analyzing evidence of change. Impact reporting is communicating that evidence to stakeholders. Impact management goes a step further, using the evidence to improve decisions and outcomes. GIIN describes this full cycle as identifying positive and negative effects, then using data to learn, adjust, and improve.

What should an impact report include?

At minimum: reporting scope, goals, key metrics, outcomes, stakeholder stories, methodology, challenges, lessons learned, and future commitments. The best reports pair quantitative data with human stories and are transparent about what is still unknown.

How often should organizations publish an impact report?

Most publish annually. Some report quarterly, after a major campaign, or after a grant period. Consistency matters more than frequency because it demonstrates ongoing commitment and allows year-over-year comparison.

How do you avoid greenwashing in an impact report?

Use specific claims backed by defined metrics, baselines, methodology notes, and honest disclosure of gaps. Include what did not work. Seek external validation where the stakes are high. If a claim cannot be supported, remove it.

Do people actually read impact reports?

Some do, some skim, and some use them as trust signals without reading closely. Nonprofit practitioners on Reddit report that concise, visual, story-led reports get more engagement, while long text-heavy documents are largely ignored. Design for the skimmer and the scrutinizer.

Is impact reporting required for B Corps?

Certified B Corps must make their B Impact Assessment scores public. B Lab’s 2025 standards require performance across seven Impact Topics with continuous improvement milestones. Whether a standalone annual impact report is required depends on jurisdiction, legal form, and certification context.

How long does a first impact report take to produce?

Expect two to four months for a first report, especially if the organization needs to define metrics, identify data owners, validate numbers, and establish methodology. Subsequent reports get faster once the process is repeatable.

Can impact reporting actually drive business results?

Yes, when it is done well. Credible impact evidence supports customer trust, investor confidence, retail sell-in, employee retention, and partnership development. The report becomes useful when it informs decisions, not when it sits as a PDF on a website footer.

Organizations ready to build an impact reporting system that connects sustainability work to real business outcomes can explore Grounded World’s Accelerate services or start a conversation about what credible impact reporting looks like for their context.